Introduction: Why Milton Keynes Should Be on Your Radar

If you are a UAE-based investor looking for a stable UK property market, you have probably wondered where to start.

A house to buy Milton Keynes might be exactly what you need. This city sits right in the middle of England, and it offers something that many other places cannot match: serious growth potential combined with great transport links.

Here is a fact that might surprise you. Between April 2025 and March 2026, the average property price in Milton Keynes was around £376,000. Over 6,200 homes changed hands in that same period, according to Plumplot data. That is a lot of activity for a city that many international buyers still overlook.

Why does this matter for you? Well, Milton Keynes is only 35 minutes from London by train. You can be in the capital faster than you can drive across parts of Dubai. The UK House Price Index shows that property values across England rose by 0.8% in the 12 months to February 2026. Meanwhile, specific parts of Milton Keynes, like the MK9 3 area, saw price growth of 3.1% in the last year alone. That is strong performance compared to the national average.

But here is the thing. Buying a home in the UK as an international investor is not as simple as booking a flight and signing papers. You face unique hurdles. Things like UK mortgage rules, stamp duty surcharges for foreign buyers, and the conveyancing process can feel confusing if you are used to buying property in the UAE. The same careful research you do when looking for a commercial property in Dubai applies here.

This guide is your step-by-step roadmap. Whether you want a house to buy in Sutton Coldfield, a house to buy Rotherham, or you want to buy house Belfast, the same principles apply. But we are focusing on Milton Keynes because it offers something special: consistent capital growth, a central location, and a market that is busy but not overheated.

By the end of this article, you will know exactly how to find, finance, and close on a property here. No fluff. Just real steps you can use.

Why Milton Keynes? A Snapshot of the City and Its Property Market

So why should you look for a house to buy in Milton Keynes instead of somewhere else? The short answer is that this city was built for growth.

Milton Keynes is not like most UK cities. It was carefully planned from the start. The city has a grid system of roads, lots of roundabouts, and more than 20 million trees. Yes, that is a real number. It is actually one of the greenest cities in the country. You get the calm of nature mixed with the convenience of a modern city.

But here is what really matters for investors. Milton Keynes is one of the fastest growing cities in the UK. The population has been climbing steadily for years. More people means more demand for housing. And more demand means your property value has room to grow.

Let us talk numbers. Between April 2025 and March 2026, the average price for a house to buy Milton Keynes was about £376,000 according to Plumplot data. That same period saw over 6,200 properties change hands. Compare that to the England average of £290,000 from the UK House Price Index. Milton Keynes is above the national average, but still far below London prices. That gives you room for better returns.

Now think about location. Milton Keynes sits right in the middle of England. It is about 35 minutes from London by train. You can be in the capital faster than you could drive across central London itself. The city also sits near the M1 motorway. That means easy road access to Birmingham, Leicester, and the rest of the country.

Here is the exciting part for future growth. Big transport projects are happening now. The East West Rail project will link Milton Keynes directly to Cambridge and Oxford. That is three of the most important cities in the UK connected by one rail line. When that opens, demand for houses in Milton Keynes could jump significantly. Investors who buy now might see very strong capital gains in the coming years.

The economy here also helps. Milton Keynes has a diverse job market. It is home to big companies in finance, tech, logistics, and automotive sectors. Companies like Jaguar Land Rover and Argos have major operations here. When people have good jobs, they want to buy homes. That supports property prices.

For buy-to-let investors, this city is a strong option. Rental yields in Milton Keynes are generally better than London. You can find properties where the rent covers your mortgage and still leaves some profit each month. That is harder to do in expensive markets like central London.

The city offers a mix of property types too. You can find modern new builds in areas like Broughton or older homes in places like Simpson. This variety means you can pick the type of property that fits your investment strategy.

When you compare a house to buy Milton Keynes with options like a house to buy in Sutton Coldfield, a house to buy Rotherham, or even a buy house Belfast, Milton Keynes stands out for its central location and transport links. The same careful research you would do for any investment applies here.

The bottom line is simple. Milton Keynes offers a stable market with real growth potential. It is not a gamble. It is a calculated choice backed by solid data and strong fundamentals.

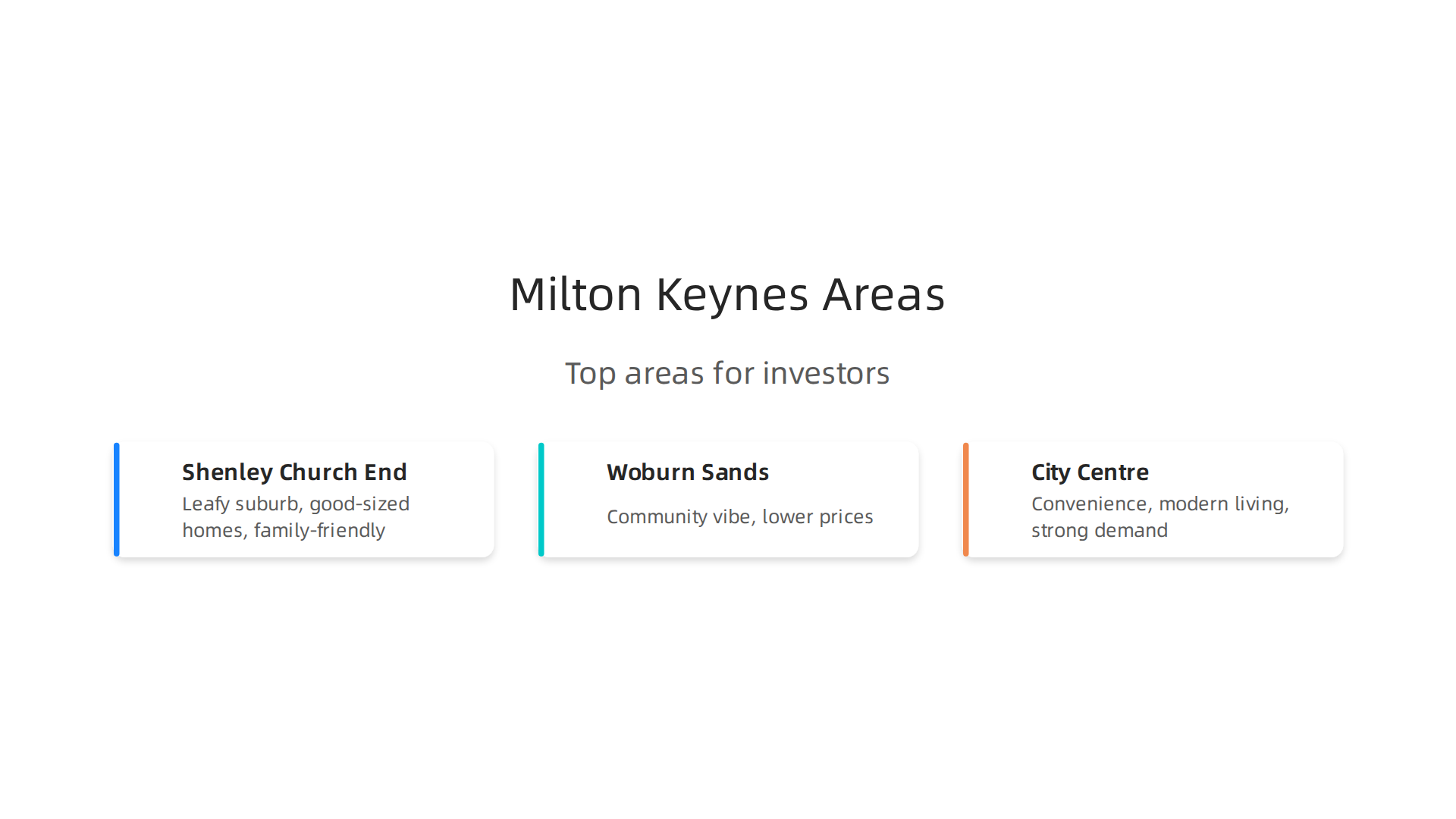

Key Neighbourhoods for International Buyers

Now that you see why Milton Keynes is a strong choice, let us zoom in on the best areas for international buyers.

Each neighbourhood offers something different, so picking the right one matters.

Shenley Church End is a popular choice for families. It is a leafy suburb with good-sized homes and gardens. The area has a village feel but is close to the city centre. Property prices here tend to be above the Milton Keynes average, but you get more space and quiet streets. It is also near St Paul’s Catholic School, one of the top-rated schools in the city. That makes it a smart pick if you plan to rent to families.

Woburn Sands sits on the eastern edge of Milton Keynes. It has a strong community vibe and a mix of older houses and newer builds. Prices are often lower than Shenley Church End, so it is a good entry point for investors. The area is close to the M1 and has its own train station, which helps for commuting.

City Centre (MK9 3) is for buyers who want convenience and modern living. You will find apartments and townhouses within walking distance of shops, restaurants, and the train station. Prices in this postcode area grew by 3.1% in the last year, according to Housemetric data. That shows strong demand for city living. The centre is also well connected to London, which is a big plus for commuters.

International investors looking for a house to buy in Milton Keynes often also keep an eye on other markets. If you are curious about commercial property opportunities abroad, take a look at our guide on commercial real estate in Dubai. It helps you compare options and diversify your portfolio.

Think about what matters most to you: school catchment, transport links, or capital growth. Each of these neighbourhoods has a clear strength. Pick the one that fits your plan.

The UK Property Buying Process: A Step-by-Step Guide for Non-Residents

Buying a house to buy in Milton Keynes from overseas might sound complicated. But the UK property process is actually quite straightforward for international buyers. The key is knowing what to expect and when.

The good news? You do not need a UK visa or residency to purchase property here. According to Experts for Expats, buying a home does not grant any immigration rights, but it also does not require them. So any non-resident can buy.

Let us walk through the process step by step.

The Timeline: What to Expect

From offer to completion, the process typically takes 8 to 12 weeks. That is the average for a straightforward purchase. But as an international buyer, you should plan for extra time.

GoGoProp notes that mortgage approval alone can take 2 to 4 weeks. And that timeline grows longer if your income is from outside the UK or your paperwork is complex. Conveyancing (the legal work) usually runs 8 to 12 weeks. HOA confirms that even with a straightforward sale, the average conveyancing time is about 12 weeks.

So if you plan to buy, give yourself a buffer of 3 to 4 months from start to finish. That way you are not stressed if things move a little slower.

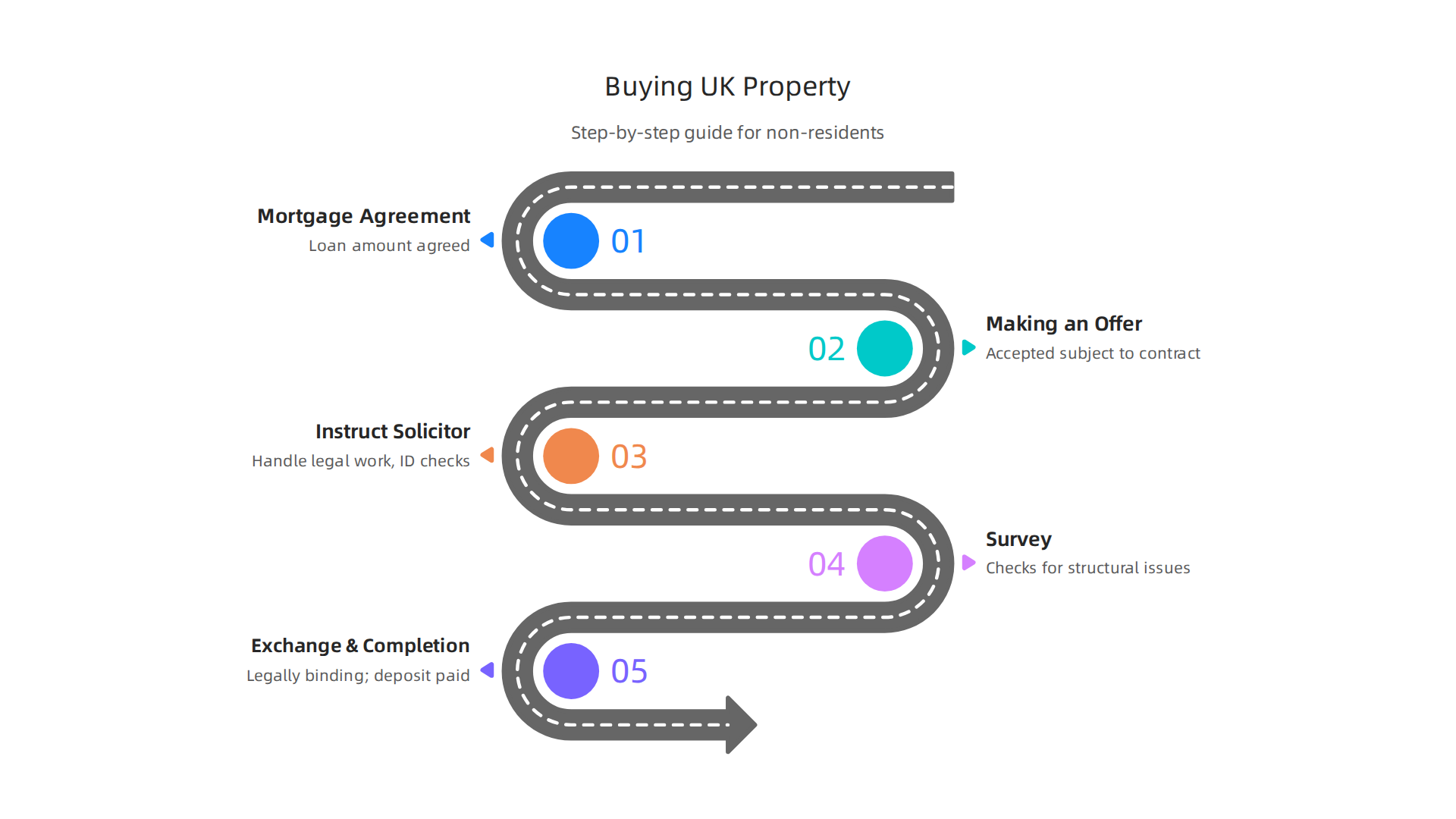

Stage 1: Mortgage Agreement in Principle

Before you even start looking at houses, get a mortgage agreement in principle. This is a letter from a lender saying they would likely lend you a certain amount. It shows sellers you are serious.

For international buyers, this step can be trickier. UK lenders may ask for more documentation if your income is in another currency. You might need to show tax returns, bank statements, and proof of employment from your home country. Some lenders specialize in expat or foreign buyer mortgages, so it is worth shopping around.

Stage 2: Making an Offer

Once you find the right property, you make an offer through the estate agent. If the seller accepts, the property is marked as "sold subject to contract." But here is the thing: in England, that offer is not legally binding until exchange of contracts. This means another buyer could come in with a higher offer and the seller could take it. This is called gazumping. MaddisonV Properties highlights that understanding the legal finality of exchange is crucial to protect your interests.

So move quickly once your offer is accepted. Do not delay.

Stage 3: Instruct a Solicitor (Conveyancer)

You need a UK solicitor or licensed conveyancer to handle the legal side.

They do the searches, check the title, handle the money, and make sure everything is legal.

For non-residents, your solicitor will also handle identity verification and anti-money laundering checks. Wise explains that foreign buyers need to provide proof of identity and address, plus evidence of where the money comes from. Have your passport, recent utility bill, and bank statements ready.

You may also need a UK bank account for the transaction. Some solicitors can work with overseas accounts, but it is smoother to have a UK one. Open it early if you can.

Stage 4: Survey

A survey is not legally required, but it is very smart to get one. A surveyor checks the property for structural issues, damp, and other problems. This is your chance to renegotiate the price if something is wrong.

For international buyers who cannot visit the property in person, a survey is even more important. You want to know exactly what you are buying.

Stage 5: Exchange and Completion

Exchange of contracts is the big moment. Once you exchange, the deal is legally binding. Both sides sign the contracts, and you pay the deposit (usually 5 to 10 percent of the purchase price). After that, you cannot back out without losing your deposit.

Completion happens a few weeks later. That is when the remaining money is transferred and you get the keys. According to MTFX, timelines vary depending on financing and other factors, so stay in touch with your solicitor throughout.

Special Considerations for International Buyers

Here are a few extra things to keep in mind:

- ID checks: Be ready to verify your identity. This is standard for all buyers but can take longer if you are overseas.

- Money laundering checks: UK law requires solicitors to confirm where your funds come from. Have bank statements and proof of income ready.

- Currency exchange: If you are buying with a different currency, watch the exchange rates. A small shift can change the price by thousands of pounds. Consider using a currency specialist to lock in a rate.

- No visa needed: Again, you can buy without living in the UK. Experts for Expats confirms that no visa or residency is required to purchase.

What Happens After You Buy

Once you own the property, you have responsibilities. You pay stamp duty (a tax on property purchases), council tax, and any service charges if it is a leasehold property. If you plan to rent it out, you will also need to handle landlord registration and tax on rental income.

The process might feel like a lot, but thousands of international buyers do it every year. Just take it one step at a time.

And if you want to explore other markets after you buy, take a look at our guide on the Dubai commercial real estate market for 2026. It helps you see how UK property compares to opportunities abroad. Diversifying your portfolio across countries can be a smart move.

Using a UK Solicitor vs. a Conveyancing Firm

So you have found a house to buy in Milton Keynes and need someone to handle the legal side. You have two main options: a solicitor or a licensed conveyancer. Both can do the job, but they are not the same.

A solicitor gives you full legal advice. They can handle complex cross-border issues, like proving where your money comes from or checking tax rules for non-residents. According to Wise, foreign buyers need to provide proof of identity, address, and source of funds. A solicitor is better equipped to manage these tricky requirements.

A conveyancing firm focuses only on the property transaction. They are often cheaper and faster for simple, local purchases. HOA confirms the average conveyancing timeline is about 12 weeks. But for international buyers, online conveyancers can feel impersonal. If you cannot visit the UK, you want someone who answers emails quickly and understands your situation.

Here is a simple breakdown:

- Solicitor – more expensive, but gives full legal support. Great for cross-border purchases.

- Online conveyancer – cheaper, but less personal. Works best if everything is straightforward.

If you are buying from overseas, pay a little extra for a solicitor. The peace of mind is worth it. And after you buy your UK property, you may want to explore other markets. Check out our guide on how to find commercial real estate in Dubai to see if diversifying across countries is right for you.

Finding the Right House to Buy in Milton Keynes

Now that you know who will handle the legal side, it is time to actually find the property. Looking for a house to buy in Milton Keynes from overseas can feel overwhelming, but the tools are better than ever in 2026. You just need a clear plan.

Start with the Big Property Portals

The first step is to browse listings online. The three biggest property portals in the UK are Rightmove, Zoopla, and OnTheMarket. They let you filter by area, property type, price range, and more.

For example, you can search for a three-bedroom house in the MK5 postcode and see everything available right away.

Rightmove has a dedicated page for estate agents in Milton Keynes where you can find local agencies like Adia Estate Agents, which has over 20 years of experience in the area. Using these portals gives you a quick feel for the market and prices. You can also save your search and get alerts when new properties appear.

Work with a Local Estate Agent Who Knows International Buyers

Portals show you what is public, but the best properties sometimes never go online. That is why you need a good local estate agent. Look for one that specifically works with international clients. They understand your timeline, your need for virtual viewings, and the paperwork involved.

Thomas Connolly is one of the fastest growing estate agents in Milton Keynes. Their agents live locally and know the area well. A local agent can give you off-market opportunities and help you move quickly when the right house appears.

If you are after a more premium property, firms like Fine & Country have a global network that specializes in prime homes. Their international reach makes them a great fit for buyers who cannot visit often. The Best Estate Agents Guide 2026 also named Alexander Lawrence one of the top agencies in Milton Keynes, so check their team out if you want a trusted partner.

Plan Your Viewings Carefully

You will want to see the property before you buy. If you can, plan a viewing trip to Milton Keynes. Spend a few days driving around different neighborhoods. Milton Keynes is famous for its grid road system and roundabouts, so getting a feel for each area matters.

But if you cannot travel, do not worry. Many agents now offer virtual tours and video walkthroughs. You can also hire a local representative to attend viewings on your behalf. A good solicitor or estate agent can recommend someone. There is a helpful YouTube video that covers the 7 experts you need to buy a UK property from abroad and it explains exactly how to set up remote viewings.

Keep an Eye on Other UK Markets Too

While your focus is on Milton Keynes, it is smart to know what else is out there. Maybe you are also thinking about a house to buy in Sutton Coldfield, a house to buy in Rotherham, or a buy house Belfast opportunity. The same search steps apply. Use the same portals, find a local agent, and arrange viewings. The process is the same, just the location changes.

The key is to be organized. Keep a spreadsheet of properties you like. Note the asking price, the postcode, and the agent contact. That way, when you find your perfect house to buy in Telford or Milton Keynes, you are ready to act fast.

Once you have a shortlist, your solicitor can do the legal checks. But first, you need to find the home. Start with the portals, then reach out to a local agent. If you can, visit in person. If not, use a virtual tour and a local representative.

After you secure your UK property, you might want to explore investments in other countries. Our guide on how to find commercial real estate in Dubai can help you diversify your portfolio across borders.

Financing Your Purchase: Mortgages and Deposits for UAE-Based Buyers

Finding the right property is exciting. But the next question is always the same. How do you pay for it?

If you live in the UAE and want to buy a house to buy in Milton Keynes, the financing process works a bit differently than it would for a UK resident. Here is what you need to know in 2026.

Expect a Larger Deposit

UK lenders see overseas buyers as higher risk. That means you will need a bigger deposit. Most non-resident buyers need to put down between 25% and 40% of the property price. Some specialist lenders may accept a lower amount, but 25% is the bare minimum in most cases.

For example, if you are looking at a house to buy in Milton Keynes priced at £350,000, you should plan for a deposit of at least £87,500. That is a big number. But it also means you start with more equity in the property from day one.

Some lenders are more flexible than others. The key is to talk to a broker who specializes in expat mortgages. They know which banks offer better terms for UAE-based buyers.

A helpful guide on non-resident UK mortgages explains exactly how the deposit requirements work for international buyers.

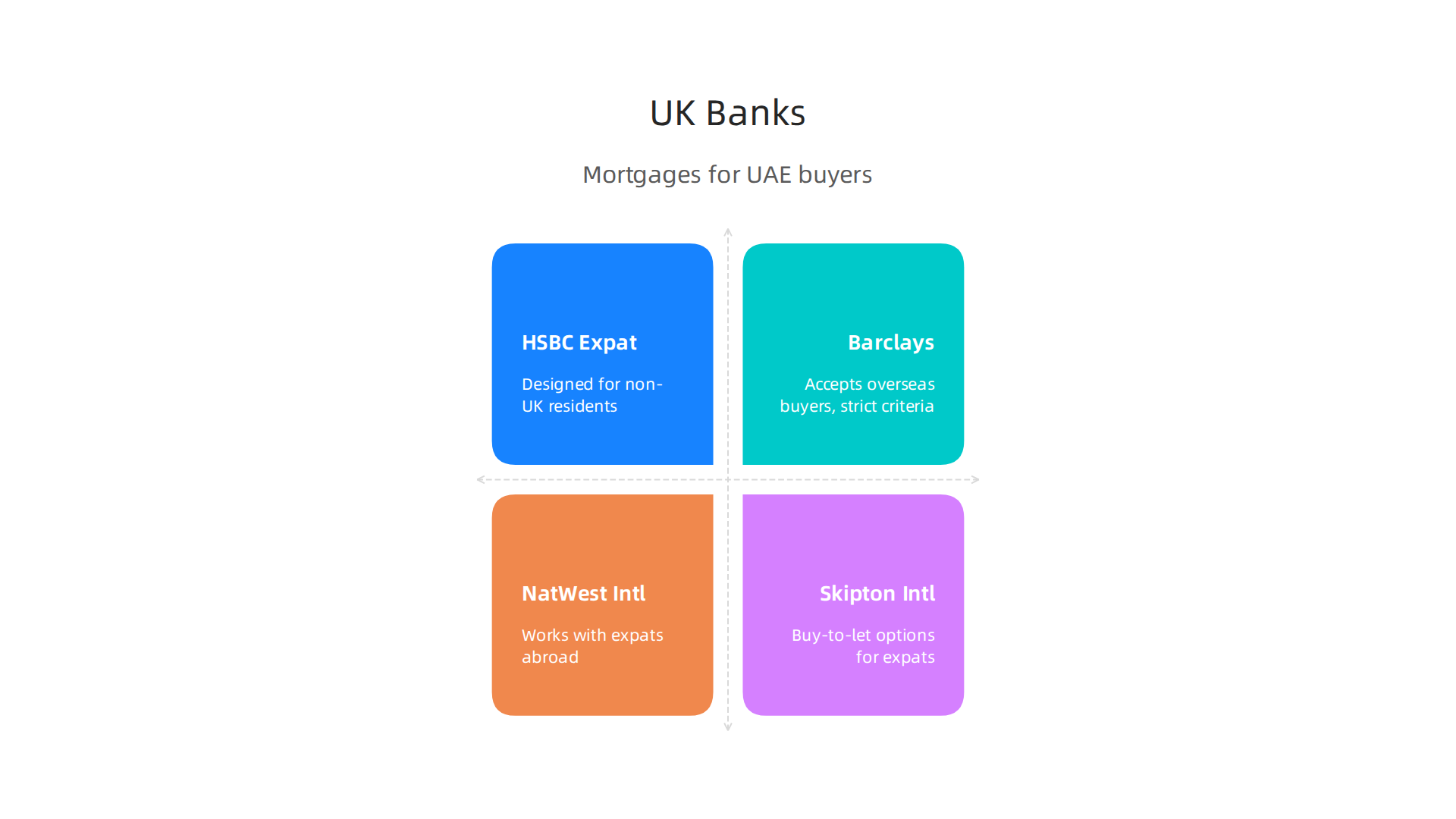

Which UK Banks Lend to UAE Residents?

Several major UK banks offer mortgages to overseas residents.

But their rules vary a lot. Here are the main ones to know:

| Bank | Notes for UAE-Based Buyers |

|---|---|

| HSBC Expat | Designed for non-UK residents. HSBC has a strong presence in the UAE, which helps. Check their non-resident mortgage page for details. |

| Barclays | Accepts applications from overseas buyers but criteria are strict. |

| NatWest International | Works with expats living abroad, including the UAE. |

| Skipton International | Offers buy-to-let mortgages for expats and non-UK nationals. See their UK mortgage options. |

Each lender looks at your income, your credit history, and where you live. You will need to prove your earnings with payslips, bank statements, and sometimes tax returns from the UAE.

A complete guide on getting a mortgage in the UK as a foreigner walks through the full process step by step.

Use a Specialist Expat Mortgage Broker

Here is something many UAE buyers do not realize. Going directly to a bank is often slower and harder. A specialist broker who focuses on expat mortgages can save you time and money.

Brokers like Expat Mortgages UK work with all the lenders that accept non-resident applications. They know which banks are offering good rates in 2026 and which ones are turning away foreign buyers.

The same logic applies if you are also thinking about a house to buy in Sutton Coldfield, a house to buy in Rotherham, or a buy house Belfast opportunity. The lender criteria are similar across the UK. The broker helps you find the right fit regardless of the city.

Watch Out for Currency Exchange

This is a big one. If you earn in UAE dirhams but buy a property in pounds, the exchange rate matters a lot. Even a small move in rates can change the final price by thousands of pounds.

Many buyers lose money by using their regular bank for currency transfers. The rates are bad and the fees add up. Instead, use a specialist foreign exchange service. Companies that focus on currency transfers for property purchases can lock in a rate and save you a significant amount.

If you need expert advice on how to handle cross-border payments, including currency exchange strategies, our detailed guide on the Dubai commercial real estate 2026 market guide for investors covers international payment logistics in a similar cross-border context.

Get Your Paperwork Ready Early

Lenders ask for a lot of documents from non-resident buyers. Start gathering these now:

- Proof of identity (passport)

- Proof of address (utility bill or bank statement from the UAE)

- Income proof (employment contract, payslips, bank statements)

- Tax returns or proof of tax status

- Evidence of your deposit funds (bank statements showing the money)

The faster you send these, the faster your mortgage offer arrives. Some lenders tell expats that the process is slower than standard UK lending. The UK expat mortgages guide explains exactly why and how to speed things up.

What If You Want to Buy in Another UK City?

Maybe you are not set on Milton Keynes alone. You might also want a house to buy in Telford or another location. That is fine. The financing steps are the same. You find a lender that accepts overseas buyers, you put down a deposit of 25% or more, and you use a broker who knows the expat market.

The only difference is the property location and price. Everything else from lender requirements to currency exchange stays the same.

Final Thoughts on Financing

Getting a mortgage as a UAE-based buyer takes planning. But it is absolutely possible. You just need a bigger deposit, the right lender, and a good broker. Do not rush. Get your documents ready, talk to a specialist, and use a currency service to protect your budget.

Once the financing is sorted, you are much closer to owning your UK home.

Proof of Income and Affordability Checks

You have your deposit ready and you know which lenders to talk to. But before any bank says yes, they need to see proof that you can actually afford the repayments. For UAE-based buyers, this means providing documents that UK lenders can understand and trust.

First, you need to show your income. That means payslips from your UAE employer, your employment contract, and bank statements showing salary deposits. Lenders usually require these to be translated into English and certified by a professional. Some lenders also ask for tax returns from the UAE, even if you live in a tax-free environment. The faster you get these documents ready, the smoother your application goes.

It also helps if you have a UK credit history. But here is the good news. You do not need one. Some lenders now accept international credit reports from agencies like Nova Credit that track your payment history in the UAE. If you have a strong record of paying bills on time in Dubai, that can work in your favor.

The same kind of documentation matters if you ever consider buying commercial property in the UAE. Our guide on commercial real estate in Dubai 2026 for leasing and buying explains the paperwork requirements for international buyers in that market.

A full breakdown of what UK lenders ask for is available in this guide on mortgages for non-residents. Check it to see exactly which documents you need to prepare.

Getting your proof of income in order early saves you time and stress. Do not wait until you find a property. Start collecting your payslips and bank statements now.

Legal and Tax Considerations for International Buyers

Your paperwork is ready, and your mortgage is moving forward. But before you exchange contracts on that house to buy Milton Keynes or any other UK property, there is another layer to understand. Taxes. For buyers living in the UAE, the UK tax system has a few surprises.

Let me walk you through the main ones so nothing catches you off guard.

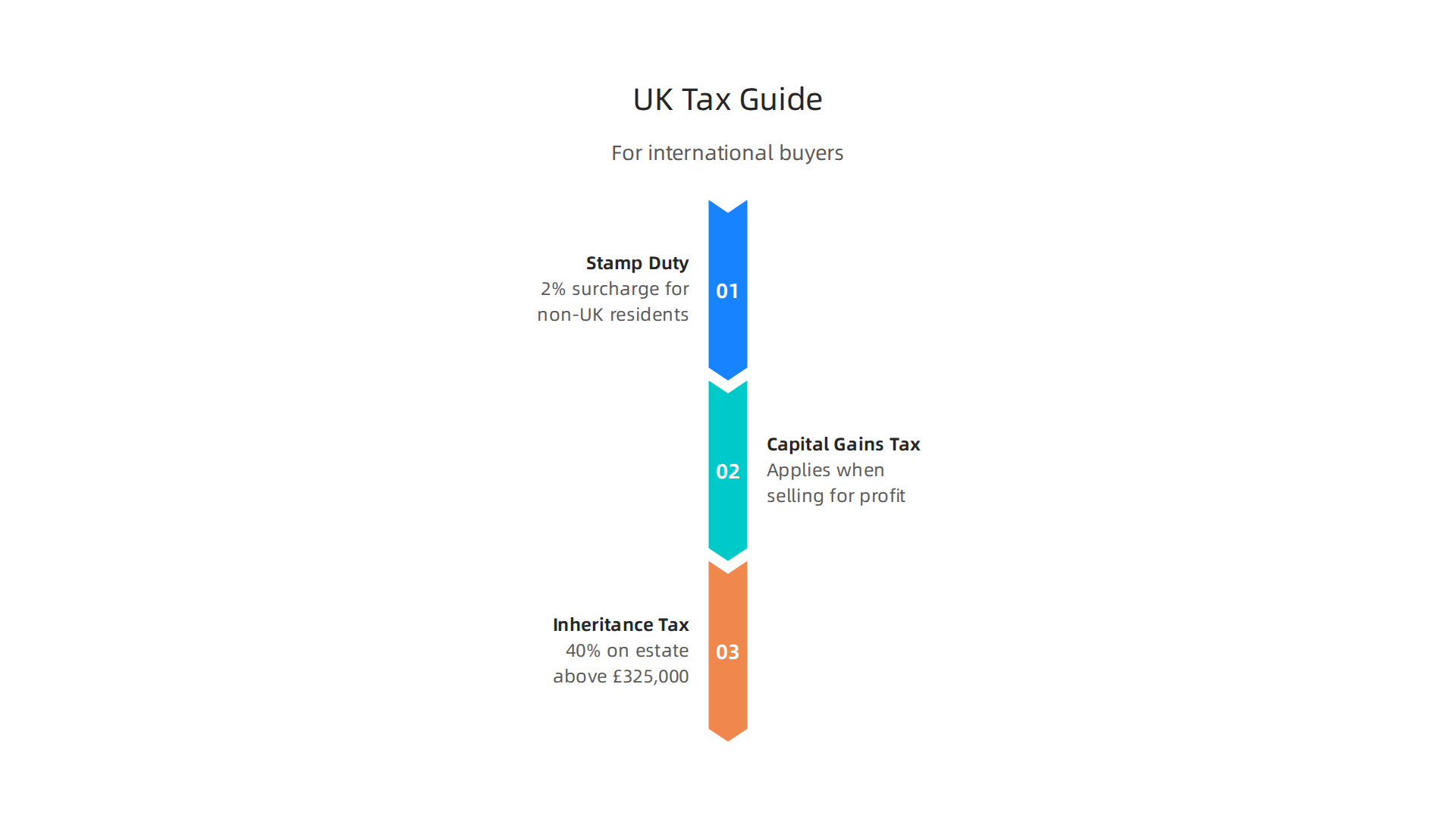

Stamp Duty Land Tax (SDLT)

Here is the biggest cost you need to plan for. When you buy a residential property in England or Northern Ireland, you pay Stamp Duty Land Tax. And as a non-resident, you pay extra.

The UK government adds a 2% surcharge on top of the standard SDLT rates for non-UK residents. This applies to all residential properties costing more than £40,000 according to the official government guidelines on SDLT surcharges. If you are also buying a second home or a buy to let property, you pay the 2% surcharge on top of the existing higher rates. A breakdown from London FS explains the surcharge clearly for 2026.

There is one piece of good news. You can claim a refund of that 2% surcharge if you move to the UK and spend at least 183 days there within a continuous 12 month period after the purchase. The Deloitte tax guide on the non-resident surcharge confirms this rule.

Use the Knight Frank overseas buyer stamp duty calculator to estimate your exact SDLT bill before you make an offer.

Capital Gains Tax (CGT)

Capital Gains Tax applies when you sell a UK property for a profit. Even if you live in the UAE and never set foot in the UK, the taxman still wants a share.

For the 2025/26 tax year, the CGT rates for residential property are 18% for basic rate taxpayers and 24% for higher rate taxpayers. These rates apply to the gain you make on the sale, not the full sale price. If you live in the property as your main home, you may qualify for Private Residence Relief which reduces or eliminates the tax. But for buy to let properties or second homes, you almost certainly will pay CGT.

Always check with a qualified tax advisor before selling. The rules can change, and the last thing you want is a surprise tax bill.

Inheritance Tax (IHT)

This one catches many international buyers off guard. If you own a UK property directly in your own name, your estate may be liable for UK Inheritance Tax when you pass away.

The standard IHT rate is 40% on the value of your estate above the £325,000 nil rate band. And here is the tricky part. The UK applies IHT to UK based assets regardless of where you live in the world. So that flat in London or that house to buy in Sutton Coldfield counts toward your estate for IHT purposes.

One common way to reduce IHT exposure is to hold the property through a trust structure. A properly set up trust can remove the property from your estate for IHT purposes. But trust law is complex, and you need professional advice from a solicitor who understands both UK tax law and international structures.

The same thinking applies if you decide to buy house Belfast or invest in house to buy Rotherham. The tax rules follow the property, not your passport.

Plan Your Tax Strategy Early

Here is the bottom line. Tax is not something to sort out after you buy. You need to factor SDLT, CGT, and IHT into your budget and your ownership structure from day one.

If you are already familiar with buying commercial property in the UAE through a corporate structure or trust, you may find similar strategies apply in the UK. For example, our guide on commercial real estate in Dubai 2026 for leasing and buying explains how holding property through a company can affect your tax position. The same principles can help you think about your UK holdings.

A good next step is to speak with a cross border tax advisor who works with UAE residents buying UK property. They can help you structure your purchase to save thousands in tax over the long term.

The house to buy Telford you are eyeing might cost more than the asking price once SDLT is added. Know the numbers before you sign.

Double Taxation Treaties with the UAE

Here is some good news after all those tax numbers. The UAE and the UK have a Double Taxation Agreement. This treaty stops you from paying tax twice on the same income. So if you earn rent from your UK property and also pay tax on it in the UK, the UAE will not tax that same income again.

This matters a lot if you are looking for a house to buy Milton Keynes or any UK rental property. The agreement covers both rental income and capital gains. For UAE residents including expats, you may be able to claim relief on Capital Gains Tax if you meet certain conditions under the treaty. The exact relief depends on your residency status and how long you hold the property.

The treaty is a big reason why UAE based buyers invest in UK property. It makes the numbers work better. You avoid the headache of double taxation on your gains or rental income.

The same logic applies if you want to buy house Belfast or check out a house to buy in Sutton Coldfield. The treaty covers all UK residential property.

If you already own commercial property in Dubai through a company, you might find this structure useful for UK property too. Our guide on commercial real estate in Dubai 2026 for leasing and buying explains how holding property through a corporate entity affects your tax position. The Deloitte tax guide on the non-resident SDLT surcharge also covers how treaty benefits interact with property purchases.

Always check with a cross border tax advisor who knows both UAE and UK rules. They can help you claim every relief you are entitled to.

Owning and Managing Your Milton Keynes Property from Abroad

So you found the right house to buy Milton Keynes. You went through the buying process. You handled the double taxation treaty. Now the property is yours. But you live in the UAE. What happens next?

The key is to set up a system before you leave. This way you avoid stress later. Let us walk through the main steps.

Get the right mortgage first.

If you plan to rent out your property, you need a buy to let mortgage. These loans work differently than a normal home loan. Lenders look at the expected rent rather than your salary. And they often charge higher interest. But they let you legally rent your home to tenants. Most UAE based buyers use a buy to let mortgage. It is the smart move.

Hire a local letting agent.

You cannot be in two places at once. A letting agent in Milton Keynes handles everything. They find tenants. They collect rent. They make sure the property meets UK safety rules.

The rules change often. An agent keeps you in line.

To find a good agent, check out local firms. Thomas Connolly is the fastest growing estate agent in Milton Keynes. They know the local market well. Another strong choice is Alexander Lawrence MK. They were named one of the best estate agencies in Milton Keynes by the Best Estate Agents Guide 2026. Both can help you manage your property from afar.

Consider full property management.

A letting agent handles tenants. A property management firm does more. For a fee of 10 to 15 percent of the rent, they cover maintenance, tax filing, and even dealing with repairs. This is perfect for busy investors. If you own a premium property, firms like Fine & Country offer management services across the UK. They have agents in over 300 locations. They can also help if you want to sell later.

Stay connected with remote viewings.

What if you need to check on your property? You can use technology. Many agents offer video tours. You can also ask a local representative to visit and take photos. The YouTube video 7 Experts you need to buy your perfect UK Property explains how to build your team. One of those experts is a property manager. They become your eyes on the ground.

The same tips work for other UK cities.

Maybe you also want a house to buy in Sutton Coldfield or a house to buy Rotherham. The management steps are the same. If you are looking to buy house Belfast or find a house to buy Telford, hire a local agent in each place. The system is repeatable.

One more thing: think about your whole portfolio.

If you already own commercial property in Dubai through a company, you might want to compare management styles. The property management world in Dubai is different. Understanding both markets helps you make better choices. Check out our guide on the Dubai commercial real estate 2026 market guide for investors to see how things work there.

The bottom line.

Owning a house to buy Milton Keynes from the UAE is totally doable. You just need the right team. Get a buy to let mortgage. Hire a local letting agent. Consider full property management. Use remote viewings to stay connected. With these steps, your property runs smoothly. You earn rental income without the headache. And you keep your peace of mind.

Summary

This guide explains why buying a house in Milton Keynes is an attractive option for UAE-based investors and walks you through the full process from search to long-term management. It covers key market data and transport links that drive demand, highlights neighbourhoods suited to different strategies, and gives a clear 8–12 week timeline for an overseas purchase. You’ll learn practical steps to secure mortgage approval as a non-resident, typical deposit sizes (usually 25–40%), and how to prepare proof of income and source-of-funds checks. The article outlines legal choices—when to use a solicitor versus a conveyancer—plus surveys, exchange and completion. It also explains important tax rules including the 2% non-resident SDLT surcharge, capital gains and inheritance tax implications, and the benefits of the UK–UAE double taxation treaty. Finally, it shows how to manage a buy-to-let from afar with letting agents or full property management and offers action-oriented tips to move quickly and avoid common pitfalls.